Cryptocurrencies were not originally conceived to be market instruments to be traded in the global financial markets. They were originally conceived as solutions to existing problems within particular ecosystems. Within the global financial sector, there exists an ecosystem which is concerned with cross-border payments and remittances.

These have traditionally been handled at the level of commercial banks and third-party money transfer companies. However, this system of global remittances and payments has been riddled with specific challenges. It is these challenges that have led to the conceptualization of a cryptocurrency known as Ripple (XRP).

So what is Ripple? Ripple is an enterprise blockchain-based solution that has been created to perform global cross-border payments. You may also call it a blockchain-based technology solution that allows users to send cross-border payments across several global payment networks. So let’s delve into this Ripple guide, without any further ado.

Origins of Ripple

Ripple is the brainchild of Ripple Labs, a San Francisco-based company which was founded in 2013 by Brad Garlinghouse, who happens to be the CEO. Other offices maintained by the company can be found in Sydney, New York, Singapore, London, Luxembourg, and India.

The Ripple company has obtained investment from several top venture capitalists such as Andreessen Horowitz, CME Ventures, Accenture, Core Innovation Capital, Seagate, Google Ventures, Santander InnoVentures and the SBI Group.

The Challenges of Today’s Remittance Systems

Conventional cross-border payment systems that have been in operation for decades have not kept pace with the rapidly evolving technologies of the 21st century. This presents the following problems to the users of these global payment systems:

a) Currency Exchange Risks

To be able to make any cross-border payments, some degree of currency conversions must be done. In countries whose currencies are internationally inconvertible, an intermediary foreign currency must be purchased and used for the transaction, and the recipient will have to convert the intermediary currency to the local currency at the destination point in order to put it to use.

This process presents several currency-based risks. Firstly, access to the intermediary currency could prove difficult, especially if there are foreign currency restrictions in place. Secondly, there is usually a ceiling on transaction amounts on cross-border payments.

Thirdly, there is a very high risk of currency value fluctuations, which could reduce the original worth of the remitted amount. This is especially telling on businesses who have to cut costs as much as possible.

b) Slow Speed of Transactions

Wire transfers are notorious for being slow and cumbersome. The process warrants the filling of boatloads of forms and can sometimes take as many as 7 days to complete. In a world where the speed of transactions is increasingly becoming desirable, such delays have become intolerable.

c) High Cost

Transaction costs of conventional cross-border payments are very high. The WTO estimates that over $1.6trillions were spent as transaction costs on cross-border payments. This makes this option of remitting money very unattractive.

d) Risk of Fiat Interventions

Ever heard of the Border Wall Funding Act which was proposed by US Congressman Mike Rogers and introduced to the House for deliberations on March 30, 2017? This bill proposed to place a 2% special tax on all remittances from the US to Mexico, Latin America, and all Caribbean countries to raise money to build US President Donald Trump’s ambitious border wall.

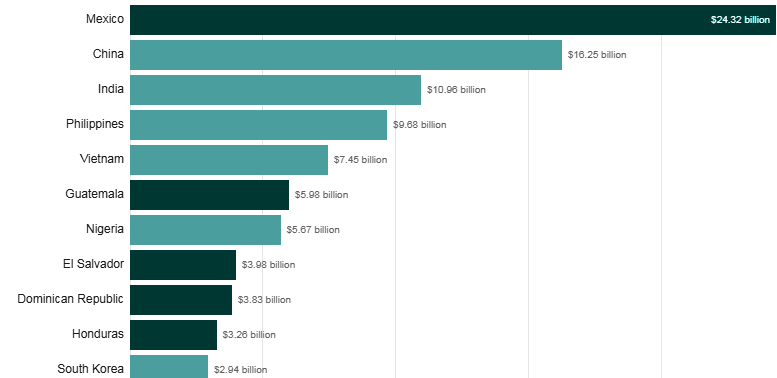

Remittances from Mexico to the US are the highest in the world ($24.32 billion).

Top Remittance Recipient Countries. (c) World Bank Group

If this bill becomes law, it will cost more to send money from the US to the affected countries. This highlights clearly how executive fiat can easily ramp up costs of cross-border payments, and it is not the only example. Already, some countries charge a Value Added Tax (VAT) on all foreign currency transactions.

Ghana charges a 17.5% VAT on all financial transactions with banks, and that includes cross-border payments.

The Ripple Solution

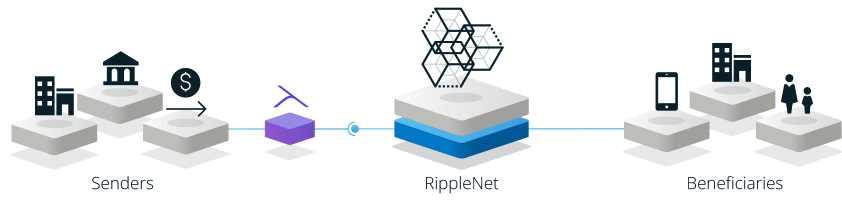

This is where the Ripple solution kicks in. Enter this new cryptocurrency, which is devoid of centralized control, accessible to everyone and has almost instant transaction speeds. Ripple is a perfect solution to the challenges highlighted above and presents this solution in the form of three products, all running on the Ripple network (RippleNet).

RippleNet will serve as an aggregating network which will connect banks, payment providers, corporate entities and digital asset exchanges, all of which will function to use the currency of RippleNet, which is Ripple. Ripple offers the following:

- Better access by offering vast connectivity across payments networks using a distributed Fintech solution.

- The speed of transactions, as settlement of payments, is done instantly.

- Funds can be traced.

- Costs are low and kept at the barest minimum.

- No fear of government interference with the process through the imposition of fees or taxes.

These characteristics are great, but are they enough to give Ripple the edge in replacing traditional methods of cross-border payments? To answer this question, Ripple’s blockchain technology has been enhanced to give it a superior edge over other existing blockchain solutions in the market. It is secure, scalable and can inter-operate with different networks.

Ripple’s Triple Offering

The Ripple solution targets three major participants in the global payments process: the banks, the businesses, and the payment providers.

a) xCurrent: Payment Processing Solution for Banks

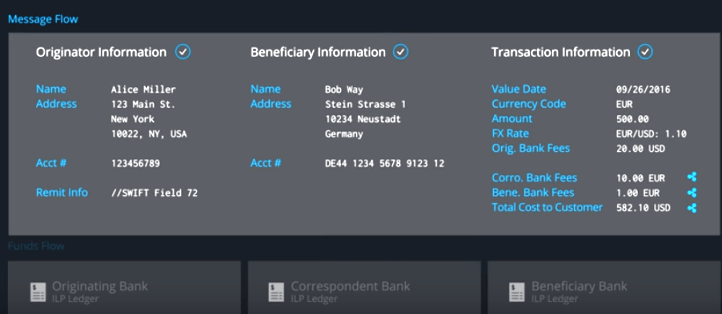

xCurrent is Ripple’s settlement enterprise software for banks, which allows them to settle cross-border payments instantly. It also comes with the enhanced ability to track transactions from point of initiation to point of completion.

xCurrent contains a messaging solution which enables the various banks involved in the transaction (initiating bank, intermediary and receiving banks) to communicate with each other in real-time to obtain payment details of the sender and receiver, obtain cost information, perform compliance checks, and confirm delivery of funds on a settlement.

Bank Wire Interface Showing Sender and bank Flow Information(c) Ripple Labs

Payments can be pre-validated even before the funds have moved. Funds flow is coordinated using the IOP ledgers of the financial institutions involved, resulting in the simultaneous release of funds at the level of each bank.

b) xRapid: Liquidity Sourcing for Payment Providers

Part of the process of cross-border money transfers involves sourcing FX from liquidity providers. This also involves some expense on the part of the banks and payment providers. In order to ensure that liquidity is accessed on demand at low cost, xRapid has been developed.

xRapid is the Ripple solution for banks and payment providers who want to reduce the cost of accessing liquidity while retaining the essential elements that make the transfer process seamless.

Cross-border payments from or into emerging markets frequently involve funding with local currencies. Sourcing liquidity from the various global liquidity providers using local currencies is expensive.

xRapid deploys Ripple to offer liquidity on demand, drastically cutting costs for payment providers (which end up being transferred to the consumer). xRapid is an enterprise solution built for banks and payment providers along the cross-border payment chain.

c) xVia: Interface for Cross-Network Payments

xVia is the software interface that allows payment providers, banks, and corporate entities to send out payments across networks. Using xVia, users can send payments to any location in the world. It also enables the capturing of information for proper documentation of such payments.

Users can process payments and track the entire process from initiation to completion. xVia also supports payment reconciliation using documents such as invoices.

Ripple as a Financial Market Asset

As is the case with other cryptocurrencies, Ripple has been listed on many exchanges and is not traded as a financial asset. It is paired with other cryptocurrencies (e.g. XRP/ETH on Binance) and also with fiat currencies such as the US Dollar (XRP/USD).

So for those who prefer to use Ripple as a trading asset on their portfolios, it is possible to buy and sell Ripple directly on exchanges or to trade the Contracts for Difference (CFD) on Ripple.

When trading Ripple as a CFD, the trader is basically speculating on the price movement of the underlying Ripple asset without actually owning the Ripple coins themselves. A discussion on how to trade Ripple in the financial markets is out of the scope of this article.

The Challenges

Ripple has been conceptualized as a cryptocurrency asset that will enable banks and payment providers perform cross-border payments at a fraction of what it currently costs to perform the same transactions using traditional means.

It was conceptualized that the massive demand and adoption of Ripple by financial institutions would drive prices up and make Ripple a valuable crypto asset for the future.

From a low of $0.0057 in July 2016, Ripple’s price stormed all the way up to $3.16 per coin on January 4, 2018. However, Ripple has suffered a major meltdown, tanking all the way to 66 cents per coin as at Tuesday, February 6, 2018.

Is it merely a market correction or is it indicative of a more serious underlying issue?

1. Competition

Competition may be a big issue for Ripple, and this competition may not be too far away. No one doubts the value that Ripple will add to the remittance ecosystem. But the question is: what is stopping a better technology from emerging a few months down the road?

Already, the Lightning Network is being developed as a system which will enhance the speeds of Bitcoin transactions to the point where it may be as efficient and as fast as Ripple.

2. Approval of Use by Central Banks

Central banks all over the world function as regulators to the banking systems in their countries. A major issue that Ripple will have is whether central banks all over the world will collectively approve the use of this technology to replace the existing SWIFT/SEPA systems of cross-border payments that have served the ecosystem for decades. Ripple Labs has made it clear that it intends for Ripple to complement and not replace the existing systems.

But what stops the SWIFT network from creating its own Ripple-equivalent network? Ripple has been adopted by less than 800 financial institutions. SWIFT is currently being used by 11,000 institutions!

SWIFT already has the industry relationships in place and if it were to create an alternative product to what Ripple is offering, it would theoretically find it easier to deploy these solutions across the global banking network a lot faster than Ripple Labs would be able to achieve.

3. Is Ripple a Decentralized Cryptocurrency?

Ripple Labs retains majority control of RippleNet with about 62% stake in the entire project. Centralized cryptocurrencies are vulnerable to regulation. The success of Bitcoin as a cryptocurrency is because no central entity controls a majority stake in the project.

Ripple Lab’s overwhelming control is a factor which remains a worry for investors. If a problem occurs with Ripple Labs, this could impact Ripple negatively.

Conclusion

Ripple has a concept which is revolutionary, but it needs to do a lot of work in order to achieve its strategic objectives totally. A major challenge is that it is coming up against SWIFT, an institution which has been operating in this space for 45 years and which could easily develop its own Ripple-like technology for quick and rapid deployment across its network of clients.

SWIFT is already being used by 11,000 financial institutions. Ripple needs to grow its existing network by as many as 100 times in order to even start to compete with SWIFT on a global scale. Ripple faces an uphill task in grabbing a substantial share of this market.

Perhaps another level of competition is going to come from outside the banking ecosystem. Some new cryptocurrency projects which intend to use telecom companies as the vehicles to drive remittances and cross-border payments using smartphones are already in development.

Time will reveal the answers to these questions.Hope this Ripple guide cleared a lot of your doubts on Ripple.

Image Courtesy: [1]