The cryptocurrency market is a strange place. It’s the only ecosystem where assets that run on a meme can turn into a multi-billion dollar industry. Because of their high potential for profit, we see all kinds of people join in. And many of them are just trying to make a quick buck. It’s also an environment of sound projects, that have brought people incredible technological advances. Blockchain technology and the protocols that are running on it are setting a new paradigm through the decentralization of almost any industry known to man.

One major advancement that unraveled before our eyes are the decentralized finance (DeFi) market. This new financial ecosystem provided individuals all over the world with access to advanced financial instruments. Moreover, it helped the unbanked finally participate in the internet economy.

However, DeFi is not without its shortcomings. It remains largely unintuitive for the mainstream population and has encountered major drawbacks regarding liquidity. It’s this latter weakness that intrigues us in this article. Some major actors in the DeFi ecosystem tried to overcome the liquidity problem by releasing a mechanism that allows protocols to own their liquidity.

We are, of course, talking about Olympus DAO and the myriad of forks that were unleashed in the market. These high-yield DAOs were supposed to solve the liquidity problem and become the basis for DeFi 2.0. But something went horribly wrong in the process. Like Icarus, these innovative platforms flew too close to the sun and soared before they crashed and burned. In this article, we analyze the concept behind the high-yield DAOs, and why they failed to deliver on their promises. Let’s begin with a short intro to what they are and how they work.

What Are High-Yield DAOs?

DAO stands for decentralized autonomous organization. In this narrative, the rules on how the organization functions (governance, voting, etc) are set up in blockchain smart contracts. DAOs usually rely on one key concept which is their shared treasury. The funds that are in this treasury can be used by the DAO in a variety of ways. And usually, the treasury requires multiple signatures from the participants to be unlocked.

For example, in our Nouns DAO review, we saw how that treasury could be used to fund various charities and social good initiatives. In the narrative of high-yield DAOs, the treasury has a goal to provide the protocol with its own liquidity.

But what’s the big deal about this?

Liquidity – The Main Issue With Decentralized Finance

As we briefly mentioned, high yield DAOs attempt to improve the current DeFi landscape by eliminating the need for mercenary liquidity providers. Before their appearance, decentralized exchanges and lending protocols required users to lock up liquidity so that they could provide their services. Then, the protocol rewarded these users with LP tokens as an incentive for this service.

However, many platforms encountered a huge issue when liquidity providers withdrew their liquidity from the smart contracts. As soon as the incentives started to diminish, liquidity providers would take out their liquidity. This would leave the platform dry of funds and unable to provide services. This in turn would result in a sharp plunge of the native tokens of the platforms.

High-yield DAOs like Olympus DAO promised to solve this issue by allowing the protocol to own its liquidity. Instead of functioning through a liquidity pools mechanism, the protocol would sell a token that acted as a bond to the treasury. Users would bond assets such as DAI or ETH and the protocol would lock up the liquidity into the treasury.

In exchange, the users would receive the native token of the platform that acted as the main incentive for providing liquidity. If the user stakes these tokens they would produce incredibly high yields. These boosted yields often equated to more than 10.000% APY, which is quite an consequential amount. In this scenario, a user staking $10 worth of tokens would have $1000 worth of rebases. Sounds a bit too good to be true, doesn’t it?

Which brings us to our next question – how did the protocol manage to provide such high yields to users that stake their tokens?

Explaining Game Theory in the High-Yield DAOs narrative

High-yield DAOs essentially rely on game theory and attempt to innovate the way people interact with financial protocols. The assumption is that the user will choose the action that benefits the protocol the most, and by projection, benefits himself the most in the long run.

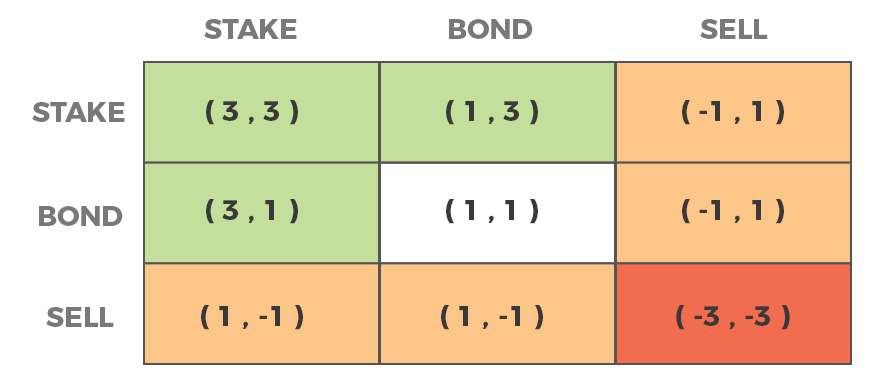

Let’s consider the three major actions that the user can overtake in the protocol: stake, bond or sell their assets. Consider the matrix below of the combination of actions two users can commit to. Each action is scored from most detrimental (-3) to most beneficial (3) to the protocol.

By now, you might have seen the (3,3) symbol in Twitter nicknames, Medium posts and memes. It represents the most beneficial action in the high-yield DAOs, where everyone stakes their tokens. This (Stake, Stake) strategy ensures that the protocol can become a stable store of value in the long run.

The (3,1) and (1,3) strategies combine bonding and staking and provide a decent positive impact as they allow the protocol to accumulate liquidity as well.

Then, the (1,-1) and (-1,1) strategies remain neutral for the protocol as they combine positive and negative outcomes.

The only true negative outcome is when both users sell their tokens at the same time (-3,-3). It represents selling pressure without any added liquidity, which threatens the system’s viability in the long term. This selling pressure can drastically impact the price of the native tokens to the downside.

However, the protocol creators believe that this scenario where everyone succumbs to selling pressure would only occur if crypto goes to zero or the users lose their trust in the system.

Quite unlikely, right?

Safeguards That Relied on Human Behaviour

Everything was set in place to prevent the doomsday scenario. The boosted yield mechanism was to counteract the price decrease and provide a stable value for the holders. Theoretically, even if the price suffers a crash, the high yields should cover the losses and keep the user in the green.

Moreover, the treasury had a goal to buy back tokens from the open market in case their price got dangerously low. This mechanism should have provided a way to stabilize the price of the high yield tokens and remove the incentive for mass sell-offs from holders.

Even so, the system needs constant liquidity flow or constant positive coordination to benefit holders and protocols and remain secure and stable. But, as you can imagine, continuous positive coordination (staking/bonding) is not realistically achievable.

What Went Wrong?

As you might have guessed by now, none of this worked. The high yield protocols relied on a utopian scenario where the individuals holding the tokens would continue to collaborate. That said, (most) humans are selfish and they quickly panic when they see the value of their capital melt before their eyes.

It doesn’t help that these protocols mainly employed a glorified Ponzi scheme to provide their high yields. They entirely relied on people trusting the system and continuously purchasing new bond tokens. But without new users bonding tokens and staking them, there was no other reliable source of income to cover the rewards.

The theory also didn’t take into account human greed. Many investors got involved only to make quick profits. And who can blame them, as the primary promise of the DAOs was incredibly high yields? Very few looked beyond this promise and understood the new archetype these DAOS were trying to set up for DeFi 2.0.

More so, greed played an additional part in the projects’ demise. Other DeFi platforms offered leveraged yield farming products using these high-yield tokens. Many holders locked up their coins in the hope to decuple their already incredible yields. However, when the prices crashed, a cascade of liquidations on these leveraged positions resulted in a literal annihilation of the token’s price.

Reaching the Point of No Return

But how did it come to this? Let’s break down the steps that brought the high-yield DAOs to a point of no return.

- Astronomically high yields are offered to draw in new liquidity from opportunistic individuals. These high yields are unsustainable in the long term but manage to gather sufficient interest in the platform and provide an upside momentum in the markets. People buy tokens and stake them, executing the best possible scenario of collaboration.

- The staking rewards start to decrease. This, in turn, pushes investors to dump their tokens as their expected yield is reduced considerably. They try to quickly capitalize on the profits they already made and avoid further rewards reduction.

- The market value of the token decreases as more people dump their tokens in the market. Investors with larger positions have no incentive to sell in small batches since they already made huge profits from the rebases.

- The number of stakers decreases. The combination of lowered yields and lowered token prices push people to sell their tokens, engaging in a vicious (Sell,Sell) circle that further shakes the foundation of the protocols.

Another factor that influenced the crash of these DAOs is time. The selling pressure got gradually worse as people lost faith in the system and the lack of cooperation slowly settled in. The price of the tokens declined, with no signs of improvement, leading to investors massively abandoning the protocols and selling their tokens at a loss.

Could the Protocol Leaders Have Prevented This?

As we previously mentioned, a mechanism was set up to prevent the price from spiraling out of control. After reaching the point of no return, the project leaders could have stepped in and chosen to do one of two things:

- Engage in buybacks and gradually raise the market value of the tokens. This could have established a new wave of trust within the community and provided incentives to hold onto their staking positions.

- Carry out airdrops directly from the treasury to token holders. This would have fairly compensated backers and once again, increased trust in the system.

However, greed once again prevailed and the large majority of projects chose to do neither of these things. Instead, the entire ecosystem of high-yield protocols opted to rug-pull the investors. They either blatantly emptied the treasury or simply purposefully did nothing and let the tokens tank in value.

Olympus Has Fallen

Olympus and its OHM token that was once valued at over $1000 has plunged under $50. Early backers lost most of their money and are now waiting for the next price increase to dump more of their tokens. The collaborative spirit is dead, as people are switching to short-term strategies to recover their losses.

What’s more, the treasury still holds over $400 million, with no sign of the team buying back tokens on the market to rectify the token’s price decline. The community relied on the promise that the team would step in and correct the price when needed. Unfortunately, this never happened and the treasury still remains in control of a 4/7 multisig wallet.

Others Followed Suit

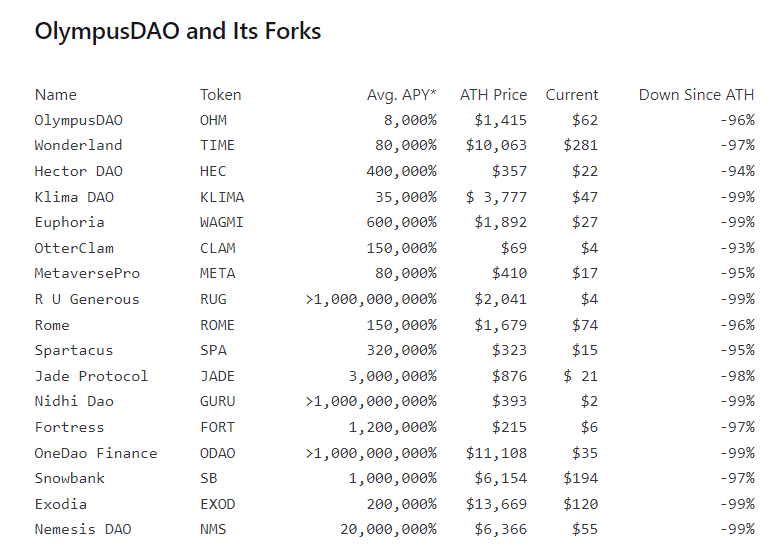

Olympus wasn’t the only protocol that failed. Its downfall was either preceded or followed by the large majority (if not all) of the copycats that provided high yields. As the market experienced a severe downturn following the peaks of November 2021, high-APY DAOs simply couldn’t survive.

Wonderland $TIME

The Wonderland protocol is worth mentioning because not only did its $TIME and $MIM cryptocurrencies crash, but it also dragged down $LUNA, one of the top 10 tokens of 2022. Many investors had $TIME leveraged positions on Abracadabra, a lending platform that commonly offers UST trading pairs.

However, UST is tightly linked to the LUNA token on the Terra blockchain. The protocol needs to burn LUNA to keep the algorithmic UST stablecoin close or equal to $1. In this case, the price of LUNA increases.

The demand for UST on Abracadabra required more stablecoin minting, and Terra burned LUNA in the process. However, once people started to pull out their $TIME leveraged positions, UST started to lose its peg to the dollar. In turn, Terra needed to create more LUNA, crashing the price of the cryptocurrency.

Klima DAO

Klima DAO is one of the ethical DAOs that attempt to use the web3 capabilities to provide a better tomorrow. Based on the Toucan Protocol, the ecosystem offers tokenized carbon credits on the blockchain.

However, instead of attracting investors and backers through genuine long-term incentives, Klima opted for boosted yields of up tp 30.000%. While the initial launch attracted a lot of liquidity, the price of the KLIMA token quickly plunged. From a high point of $3700, KLIMA is now trading under the $20 mark and is one of the Olympus forks that have lost the most value.

Concluding Thoughts

Olympus had a decent idea – to provide DeFi protocols with their own liquidity. However, this concept heavily relied upon people trusting the system. It didn’t take into account that the high yields would mostly attract the wrong kind of investor.

The core community believed that Olympus or its forks could genuinely improve the DeFi ecosystem. However, the vast majority of the high-yield DAO participants were speculators that wanted to make quick profits.

What’s even more interesting is that this total annihilation of these protocols could have been prevented by the users themselves. If people didn’t start massively selling their high-yield tokens, the price could have declined gently and would have let the yields cover the losses. Nevertheless, emotions, and more specifically, panic took over and the rest is history. Also, if the protocol owners that control the treasury stepped in at the right time, the experiment might have been successful after all.

With all that in mind, we can’t ignore the fact that liquidity ownership is a crucial concept in the evolution of the DeFi ecosystem. If incentives remain realistic, we could see another round of these DAOs appear, with a more sustainable solution for the long term. Hopefully, we will see this concept implemented in a better way, with the hard lessons learned from the past taken into account.